I left for my holidays at the start of the summer, with bond yields going down and equities performing strongly. But what a difference a summer can make. Bond yields have gone up, and equities are becoming more volatile. The market is shifting.

With a rather momentous summer behind us, I and the rest of the investment committee have debated these crosscurrents and their implications on how we invest our clients’ money. In short, with volatility looking set to continue, we have decided to stay defensive in portfolios. However, this volatility also presents opportunities along with a range of risks. Therefore, the investment committee has agreed on three actions to mitigate the former and seize the latter.

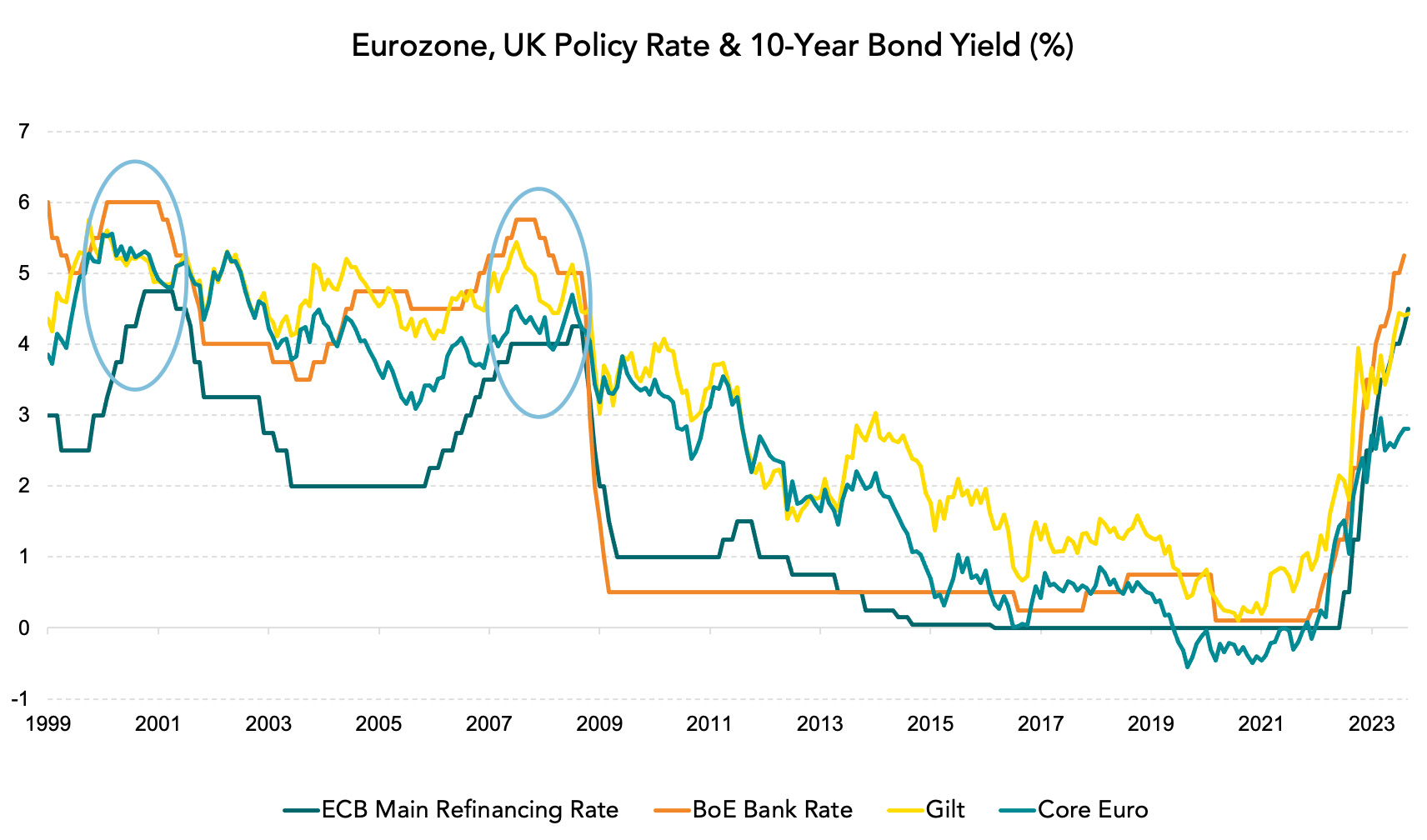

The first action is in response to the likelihood of a Eurozone and UK recession, which makes government bonds more attractive. Why? Because of the chain reaction a recession can have on bond yields. As growth slows and economies enter recession, central banks can provide stimulus by cutting interest rates. As interest rates fall, so do government bond yields. However, inflation is critical here because, as we know, spiralling inflation does not come with low interest rates. The good news is that Eurozone inflation has decisively moved past the peak, and UK inflation is also trending down, though not as much as in the Eurozone and the US. This fall in inflation means we’re close to the peak in interest rates. Therefore, we believe now is an opportune moment to capture the yield of Eurozone government bonds before central banks cut rates in 2024 to stimulate economic growth.

The second action is in response to the underwhelming rebound of China, impacting our Asia-Pacific equities position, which includes Japan. The pick-up we expected from China this year hasn’t happened. Many factors contributed to this, which we explain in our Investment Focus section below. Ultimately, the investment committee agreed that it’s unlikely we’ll see a swift turnaround in the fortunes of Chinese and broader Asia-Pacific equities. One bright spot in the region has been Japan. But the rally has been driven by the lower-quality part of the market; valuations are no longer cheap, and we think investors understand the reform and rebound story well. So, we’ve closed our position in Asia-Pacific equities and reorient it towards developed market equities.

The third action is that we’ve lowered the probability of a US recession in our forecasts, which nevertheless remains a likely outcome. If a recession does hit the US, the economic resilience we’ve seen so far suggests it’s likely to be mild. This matters because it implies that dividend cuts are less likely than we previously thought. So, the investment committee has agreed to shift our US dividend equity exposure back towards the broader US market.

Finally, as an Italian, I should mention the Rugby World Cup. We started the campaign with a record victory in the opening round, and I say this not to brag but as a reminder that, like a rugby game, the momentum in markets can shift quickly. This is why it’s crucial to stay focused on the long term and build a diversified team (or portfolio) with a broad range of attributes that can weather a range of storms. I discuss this in my latest House View blog post on portfolio diversification.

.png?width=400&resizemode=force)