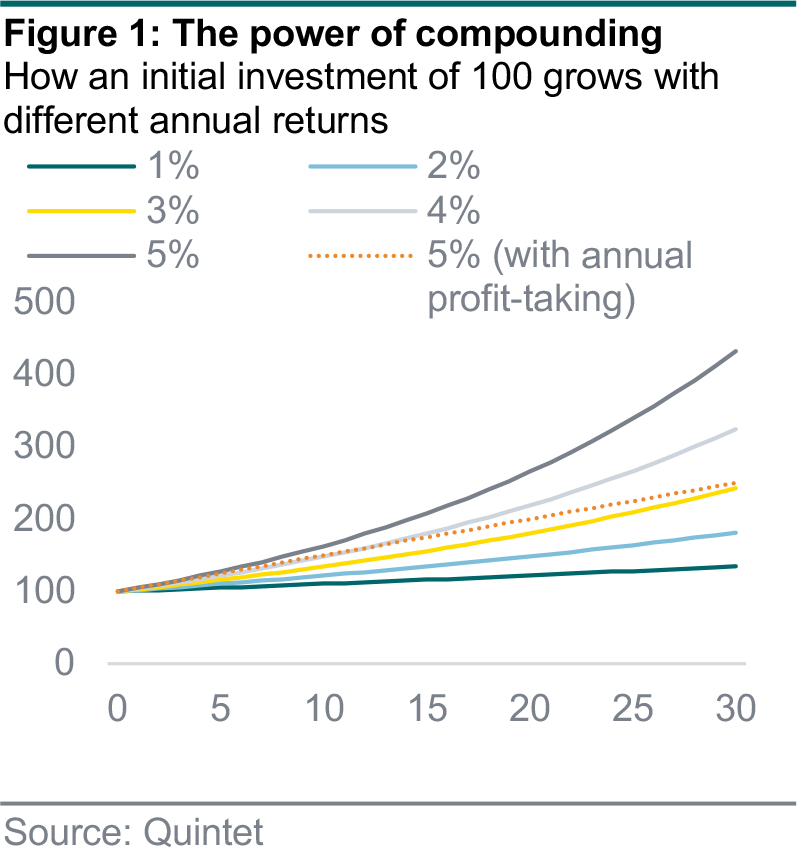

We believe the best way to achieve your financial goals is by investing in financial markets with a long time horizon. That’s because the compounding effect is so powerful, where the value of your portfolio is magnified as the returns build up over many years (figure 1).

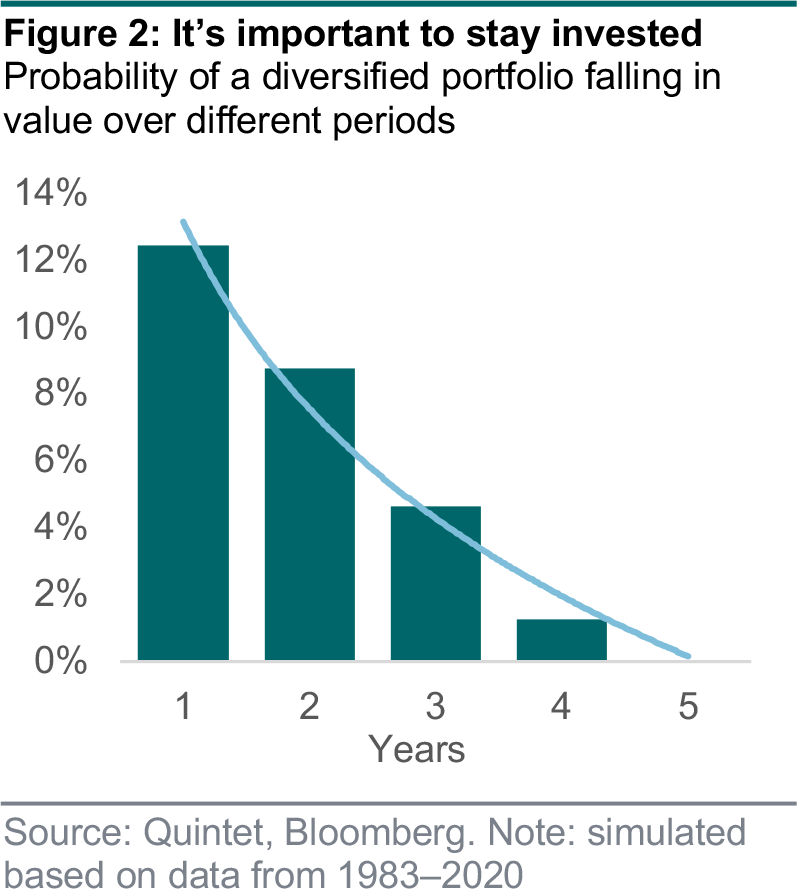

In order to benefit from compounding, it’s important to stay invested through periods of strong and weak market performance, as well as low and high volatility, without succumbing to the temptation to either take profits or capitulate and crystalize losses. Indeed, staying invested in a well-diversified portfolio over time pays off – in the past the likelihood of a negative outcome has decreased the longer the time horizon (figure 2).

Staying invested through good and bad times is only realistic if you are comfortable with the level of risk in your portfolio — too little risk and returns will underwhelm; too much risk and drawdowns will be unbearable. Therefore, it is critical that the long-term portfolio we recommend matches your risk appetite, return expectations and tolerance for losses.

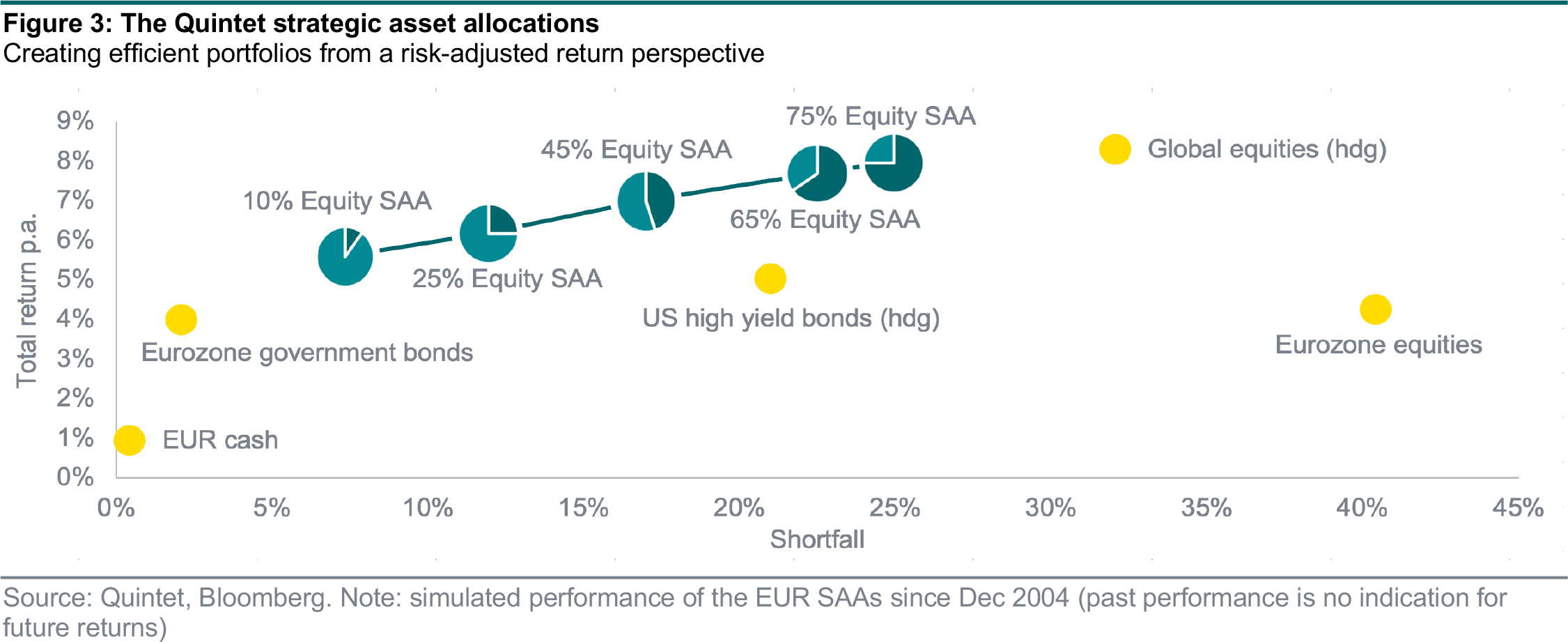

We all have different tolerances to risk. In order to meet a wide range of different objectives, we define a set of long-term asset allocations that span the risk tolerance spectrum, from low to high. We call them the Quintet strategic asset allocations (SAAs) (figure 3).

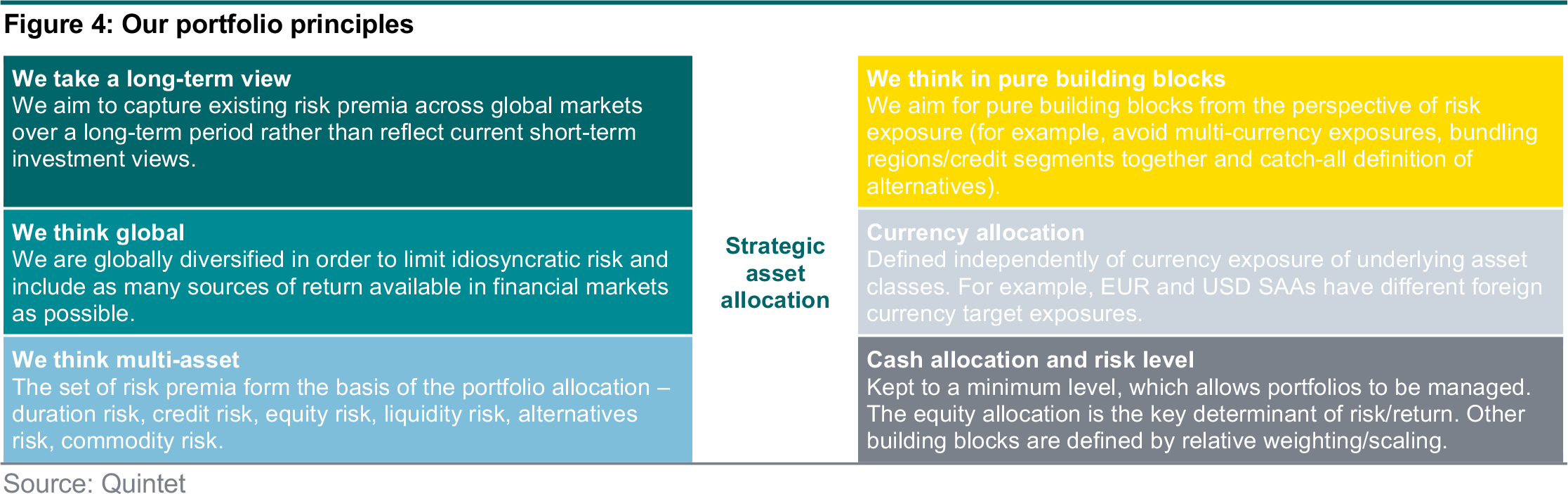

We define our SAAs with a single objective in mind — find the allocations with the highest expected return for a given level of risk. In other words, we’re looking for the most efficient portfolios from a risk-adjusted return perspective. To do so, we combine our two core investment beliefs — global diversification and sustainable investing (SI) — with a set of portfolio principles (figure 4).

More specifically, to find the right SAAs for you we go through the following five steps:

Global diversification in equities and bonds

We take a global approach to our asset class universe and believe portfolios should be geographically diversified for two main reasons:

You might prefer to invest in companies or regions you feel you know, even if that means giving up potential returns. Although it’s human nature to prefer what’s familiar, there’s a negative side effect beyond foregone performance — less well-diversified portfolios are often riskier and suffer larger drawdowns. Higher risk with similar (or even lower) returns is the very definition of inefficient portfolios.

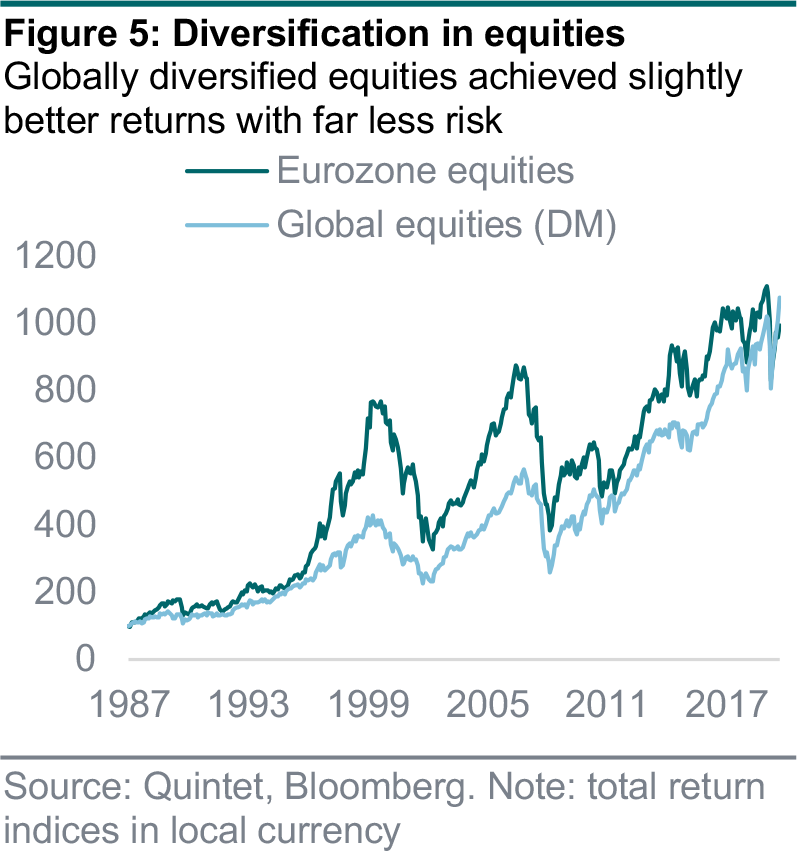

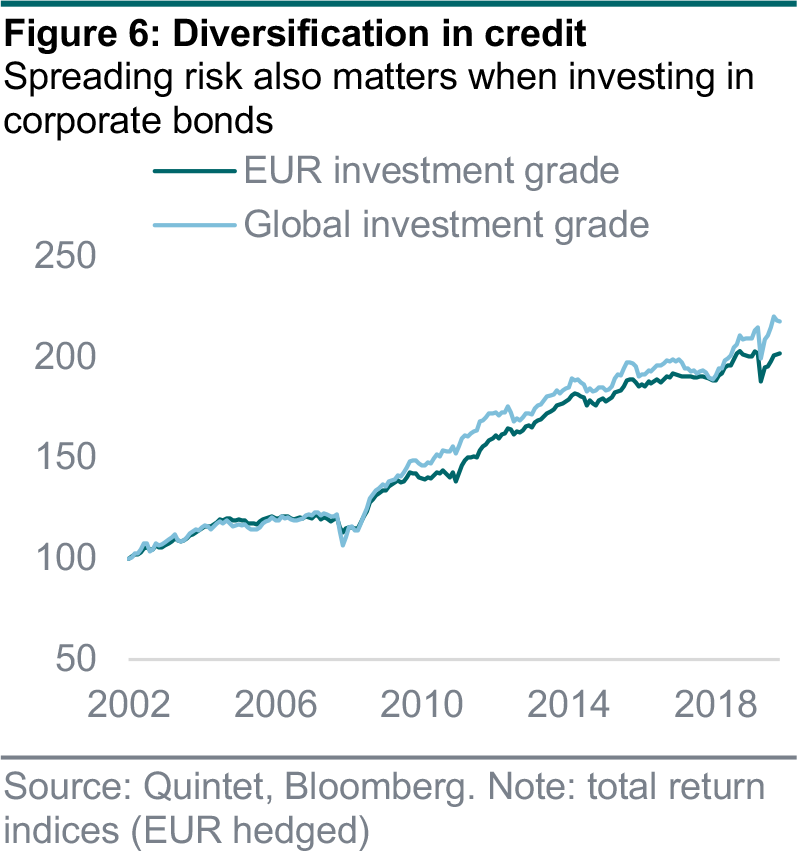

We see this happen with undiversified equity and bond exposures. For example, outsized allocations to European equities or corporate bonds achieved significantly worse risk-adjusted returns than global equities or credit over longer time periods (figures 5 and 6).

Our well-diversified SAAs help you overcome home bias and ultimately generate better results. If you still want to put a larger emphasis on a specific equity market, you can do so by allocating a smaller portion of your wealth to a dedicated stock portfolio, while keeping most of your investments in one of our SAAs.

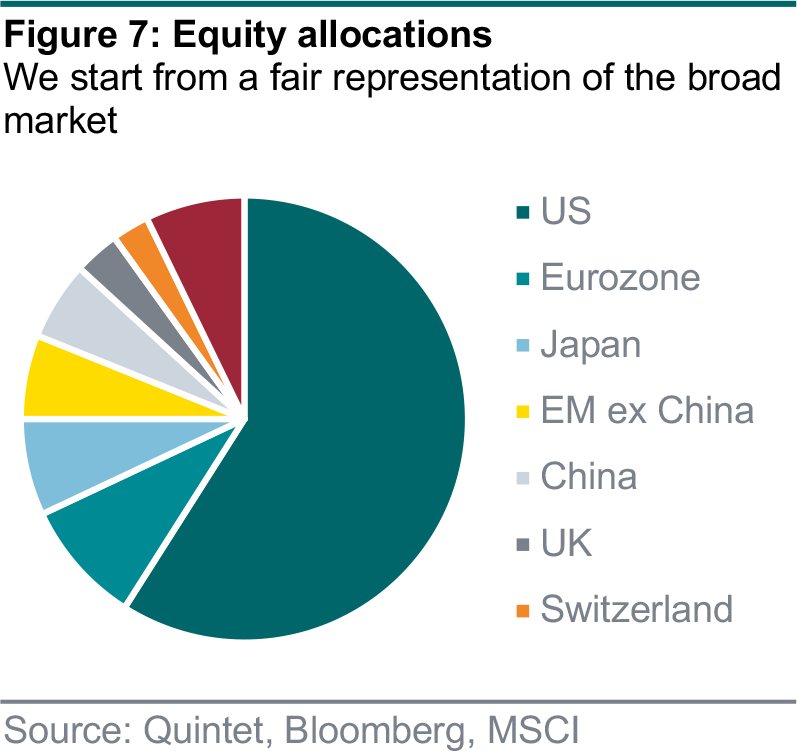

When constructing our SAAs we follow the principle of global diversification by taking the global market-cap weights of a given asset class (such as global equities) as a starting point. This ensures we start from a fair representation of the broad market, which evolves dynamically over time with the relative growth of the sub-markets (for example, US, European or Chinese equities).

We then run our CMA and optimizer models and check if there is material reason to deviate from the market-cap weights. Our most recent results led us to keep the regional equity allocation aligned to market-cap weights. Specifically, that means a larger allocation to US stocks than other regions (figure 7).

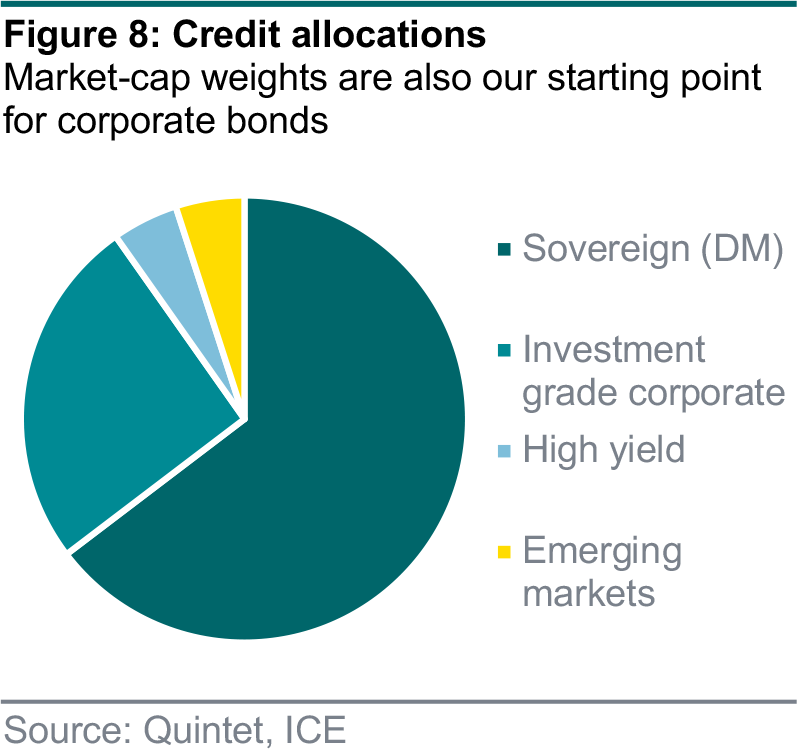

Within fixed income, we overweight global credit in our SAAs against its market-cap weight.

Developed market government bonds make up more than 60% of the global fixed income market (figure 8). But expected risk-adjusted returns for this sub-asset class are substantially lower than in the past and warrant a reduction in favor of more attractive credit sub-asset classes. We will explore this important topic in more detail in the next edition of this SAA series, to be published later in the month.

The acceleration in both infections and, to a lesser degree, hospitalisations has worried policymakers across Europe. They have reacted by reimposing restrictions on gatherings (mostly), mobility (somewhat) and activities (selectively). Whereas the first virus wave resulted in full-blown lockdowns, this time governments have taken a more flexible approach. These so-called circuit breakers have been successfully used by Israel, for example, to quickly contain the spread of Covid-19 while mitigating the economic fallout.

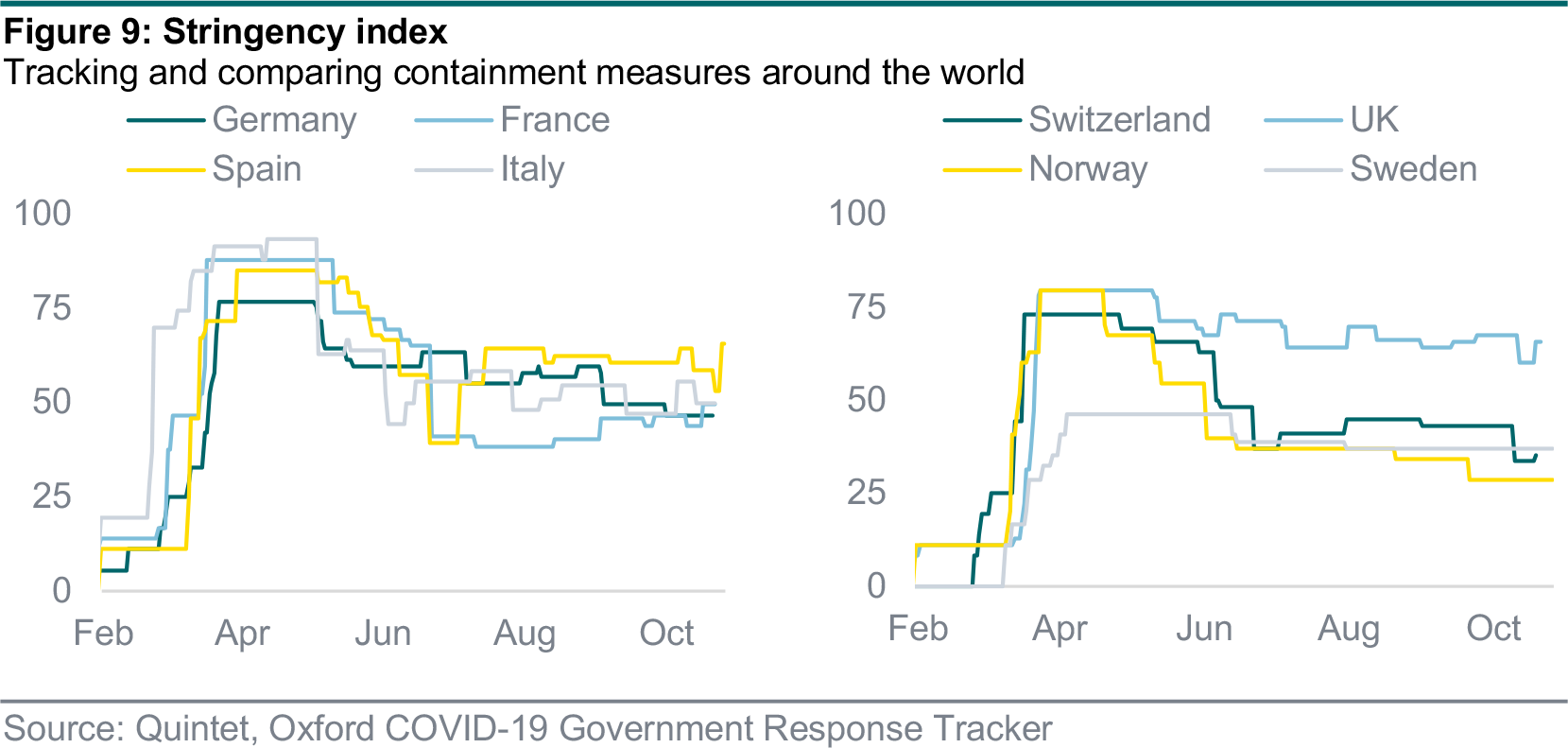

We monitor these circuit-breakers with the help of the University of Oxford’s Coronavirus Government Response Tracker. The stringency index represents the severity of the containment measures implemented (such as schools and offices closing, and restrictions on social gatherings) in a standardised way, but without judging the effectiveness.

The charts in figure 9 show that, with the exception of the UK, containment measures have eased significantly from the peak, while some countries like Spain and France have imposed tighter restrictions recently. Last week’s announcements by Chancellor Merkel and President Macron are not yet reflected in the data, and so we would expect measures to tighten, though not yet at the level of the first wave.

The weakening and stagnation in real-time and coincident indicators seen recently are likely to continue, based on the partial lockdowns introduced last week. This means that, although we expect the recovery to continue, it is likely to slow and hit a setback this quarter, with some countries to possibly show no growth or even slightly contract for a short period of time, but not suffer the deep recession of the second quarter of this year.

Export and manufacturing-driven economies (notably China and Germany) should be more resilient and able to bounce back more quickly from the containment measures. The recovery in the global industrial cycle, plus the fact that factories are now open, along with China’s pick-up, should cushion the blow for European manufacturers. Domestic and services-driven economies (notably the UK and France) are likely to see greater impacts on activity. The resilience of the US, despite its reliance on services, is probably due to the greater policy stimulus.

Carolina Moura-Alves - Group Head of Asset Allocation

Philipp Schöttler - Cross-Asset Strategist, Group Chief Investment Office

Daniele Antonucci - Chief Economist & Macro Strategist

This document has been prepared by Quintet Private Bank (Europe) S.A. The statements and views expressed in this document – based upon information from sources believed to be reliable – are those of Quintet Private Bank (Europe) S.A. as of November 2, 2020, and are subject to change. This document is of a general nature and does not constitute legal, accounting, tax or investment advice. All investors should keep in mind that past performance is no indication of future performance, and that the value of investments may go up or down. Changes in exchange rates may also cause the value of underlying investments to go up or down.

Copyright © Quintet Private Bank (Europe) S.A. 2020. All rights reserved